500 읽음

Political Market Support Today Could Become a Pension Crisis Tomorrow

0

0

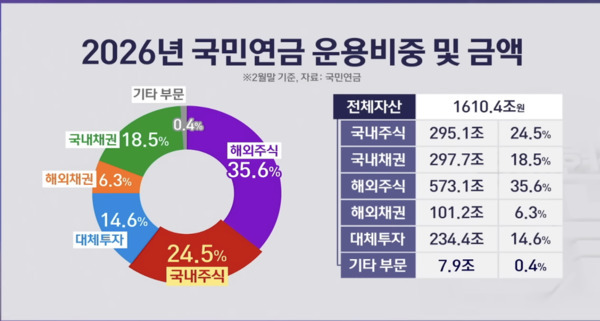

The fact that South Korea's National Pension Service (NPS) now holds nearly 500 trillion won in domestic equities, with the allocation approaching 30% of its portfolio, is not a normal way to manage retirement assets.

The first principle of pension fund management is risk diversification. Just as the old saying warns against putting all your eggs in one basket, retirement assets should be spread across domestic and international markets to protect citizens' savings during times of crisis.

Yet the NPS Fund Management Committee has effectively abandoned this principle. It raised the target allocation for domestic equities from 14.9% to 20.8% and significantly widened the permissible range. In practical terms, the rules have been loosened to allow domestic stocks to absorb as much as nearly 30% of the portfolio.

The reason is obvious: political pressure tied to government approval ratings and state-directed financial management.

When a particular asset class grows excessively large within a portfolio, pension funds are supposed to engage in rebalancing—selling assets to lock in gains and reduce risk. This is standard investment practice.

However, concerns that "the pension fund will crash the stock market by selling shares," combined with political pressure from the government, have prevented the fund from carrying out the sales it should be making. Instead of functioning as an independent investor, the pension fund has effectively become a buyer of last resort for the domestic stock market.

As a result, whenever foreign investors unload massive amounts of Korean stocks and leave the market, the burden of absorbing those sales falls squarely on the National Pension Service. Pension money fills the gap left behind by foreign capital, artificially supporting stock prices.

Retirement savings accumulated penny by penny by ordinary citizens are being used as an emergency firefighting tool to counteract market forces and sustain government policy objectives.

We must now confront the worst-case scenario.

If foreign selling continues unabated, or if an external shock triggers a major collapse in the Korean stock market, who will be responsible for the enormous investment losses?

The answer is simple: no one.

Under current law, there is no provision requiring the government or pension executives to compensate for losses incurred by the National Pension Service. The administration that applied the pressure will eventually leave office. The executives who approved aggressive investment policies will move on as well.

The bill for any market collapse will ultimately be paid by future generations through pension depletion and higher contribution burdens. The pain will fall entirely on ordinary citizens.

Those who exercise power bear no responsibility, while citizens who hold no power are left carrying all the consequences. This contradiction lies at the heart of government-directed financial intervention through the pension system.

Leading public pension funds around the world take the opposite approach because they understand the dangers of such a path.

Major institutions such as California Public Employees' Retirement System (CalPERS), Canada Pension Plan Investment Board (CPPIB), and APG (APG) follow strict global diversification strategies to avoid excessive correlation with their domestic markets.

Many limit exposure to their home markets to single-digit percentages or maintain minimal domestic allocations. Whether markets surge or crash, assets are bought and sold according to predetermined rules rather than political considerations.

This discipline is possible because their governance structures are independent from government control and managed by professional investment organizations insulated from political pressure.

South Korea's National Pension Service, by contrast, remains overseen by a Fund Management Committee chaired by the Minister of Health and Welfare, with substantial government representation.

The structure itself leaves the institution vulnerable to political influence. When pressure arrives from above, management is more likely to act as an instrument of government policy than as a shield protecting beneficiaries' interests.

The most alarming reality is that South Korea is aging faster than almost any other country in the world.

In the near future, the National Pension Service will inevitably face a "Sell Korea" moment, when it must liquidate trillions of won in domestic equities every month to meet pension obligations for a rapidly growing elderly population.

Refusing to diversify overseas assets today because of concerns about current stock market performance is merely postponing the problem while making it far worse.

When the pension fund eventually begins selling large volumes of Korean stocks to finance benefit payments, the domestic market may struggle to absorb the shock. The very policy of using pension assets to support stock prices today risks planting the seeds of a much larger market decline tomorrow.

The Lee Jae-myung administration should immediately halt any market intervention that relies on pension assets and reform the Fund Management Committee into an independent body led by private-sector investment professionals.

If government-directed financial management continues to treat the retirement savings of millions of citizens as a tool for protecting political achievements and short-term market performance, those responsible may ultimately face harsh judgment from both history and the public when the consequences arrive in the form of capital-market disruption and pension instability.

jinannkim@gmail.com

#NationalPensionService #PensionReform #KoreanStockMarket

* This article has been translated by ChatGPT.